Sweden gave data centers a

97% tax cut.

Then took it back.

The evidence Sweden hopes you’ll never see.

What is your situation?

Select the option that best describes you

You were forced out.

You’re still fighting.

The 97% tax cut can be restored.

Before committing capital, understand what happened to the operators who came before you.

Three phases. One pattern.

Phase 1 — Reinterpretation

2018. Colocation operators excluded overnight by administrative interpretation. Hyperscalers kept full benefit. Never challenged in court.

Phase 2 — Abolition

2023. Sweden removed tax benefits from data centers while keeping them for manufacturing. 65x higher tax. Only EU/EEA country to abolish.

Phase 3 — Backpedal

2024. Sweden withdrew from the Energy Charter Treaty — removing yet another safety net for investors and strengthening the case against them.

Planning to invest in a Swedish data center? Three things you must do first.

1. Structure through a BIT jurisdiction

Route your investment through a country with an active bilateral investment treaty with Sweden. Keep treaty protection in your pocket.

2. Get a preliminary ruling (förhandsbesked)

Lock in your tax position with a binding decision from Skatterättsnämnden before deploying capital. This is the single most important step no operator took in 2017.

Five claim categories.

Each claim category can be pursued through one or more legal channels — EU Commission, Energy Charter Treaty arbitration, bilateral investment treaties, or preliminary tax rulings — depending on the investor’s nationality and corporate structure.

Energy Tax Damages

Discriminatory exclusion from the 97% energy tax reduction. Colocation operators lost eligibility while hyperscalers kept full benefit (2018–2023).

VAT Recovery Claims

Non-refund or incorrect refund of input VAT on mining and data center operations. The Hedqvist ruling created a paradox that Skatteverket exploited.

Claims Against Advisors

Law firms and tax consultants who provided incorrect strategies — contributing to an estimated €100M in VAT leaks and triggering disputes against their own clients.

Claims Against Landlords & Local Partners

Landlords took your equipment. Local partners broke their contracts. Foreign investors had no effective recourse in Swedish courts.

Preliminary Tax Rulings

HFD 2022 Ref. 5 confirmed that cryptocurrency mining qualifies as “datorhall.” Investors can now secure a binding förhandsbesked from Skatterättsnämnden before deploying capital — locking in your tax position before Skatteverket changes the rules again. Projekt Datorhall helps you obtain one.

Parallel pathways. One coordinated campaign.

Despite 8 years of documented discrimination, no systematic legal challenge has ever been filed. Not by affected operators, not by industry bodies, not even by the European Data Centre Association (EUDCA). Only political disputes, industry complaints, and parliamentary debates. Projekt Datorhall changes that — deploying claims across five complementary legal channels where each pathway reinforces the others.

European Commission Complaint

The 2018 reinterpretation created a selective advantage for hyperscalers under Article 107(1) TFEU. The original GBER Article 44 framework required equal treatment. The 2023 abolition introduced sectoral selectivity against data centers while preserving benefits for manufacturing. Neither modification was notified to the Commission — a procedural breach under Article 108(3) TFEU.

Energy Charter Treaty Claims

Data center infrastructure is fundamentally dependent on electricity consumption and energy pricing. The Energy Charter Treaty protects investments in energy-related economic activities. Claims include: fair and equitable treatment, indirect expropriation through regulatory reversal, and discriminatory measures against foreign investors.

Sweden withdrew from the ECT in 2024 — but the 20-year sunset clause protects investments made before withdrawal until 2044.

In May 2025, the Swedish Supreme Court confirmed in T 555-24 that ECT arbitration remains valid for non-EU investors — directly supporting the Swiss SPV structure.

International Investment Treaties

Depending on investor nationality and corporate structure, bilateral investment treaties (BITs) between Sweden and the investor’s home state may provide additional investment protection. Sweden maintains active BITs with numerous countries. Multiple Projekt Datorhall members have structures that may qualify for BIT protection.

Eligibility assessed on a case-by-case basis depending on investor nationality and corporate structure.

Francovich Damages

Compensation claims in Swedish courts for breach of EU law. Under the Francovich doctrine (Cases C-6/90 and C-9/90), Member States are liable for damages caused to individuals by infringements of EU law attributable to the state. Three conditions: (1) the EU rule infringed confers rights on individuals, (2) the breach is sufficiently serious, (3) direct causal link between breach and damage.

Legal basis: Articles 107, 108, 49 and 56 TFEU. Sweden’s discriminatory tax measures — affecting an entire industry segment with quantifiable losses — meet the “sufficiently serious” threshold.

Administrative Court Ruling (Förhandsbesked)

HFD 2022 Ref. 5 confirmed that cryptocurrency mining qualifies as “datorhall” under the Energy Tax Act — overturning Skatteverket’s interpretation. The same reasoning applies to colocation. A new preliminary ruling (förhandsbesked) from the Tax Board (Skatterättsnämnden) would establish binding legal certainty before capital is committed.

Lesson from 2017–2018: no operator secured a preliminary ruling before investing. Projekt Datorhall ensures this mistake is not repeated.

Strategic interaction between pathways

All legal avenues are not mutually exclusive. Arguments raised in EU state aid proceedings generate factual findings relevant for investment arbitration. A Commission finding of unlawful state aid directly strengthens Francovich damages claims in Swedish courts by establishing the breach. A successful preliminary ruling establishes legal certainty that strengthens all other pathways. If Sweden justifies the abolition based on energy policy, this strengthens the argument that data center investments fall within the scope of the Energy Charter Treaty. Multiple forums prevent Sweden from ignoring a single complaint and create comprehensive pressure for resolution.

Key authorities and precedent relied upon.

Multiple CJEU and Swedish Supreme Administrative Court rulings have found against Skatteverket on related tax questions. These precedents support claims across all five legal pathways. The colocation exclusion has not yet been the subject of a formal challenge.

Högsta domstolen T 555-24 (2025)

Swedish Supreme Court, 26 May 2025. ECT arbitration remains valid for non-EU (third-country) investors even after CJEU Komstroy (C-741/19). A Swiss-resident investor’s ECT claim against Poland was upheld, while EU-resident co-investors’ claims were invalidated as contrary to EU law. Direct validation of the Swiss SPV strategy — operating from outside the EU preserves access to ECT arbitration that EU-based claimants cannot use.

HFD 2022 Ref. 5

Högsta förvaltningsdomstolen (Supreme Administrative Court), 2022. Sweden’s highest administrative court overturned Skatteverket’s interpretation of the Energy Tax Act (lagen om skatt på energi, LSE). Key holding: cryptocurrency mining constitutes “datorhall” (data center) under Chapter 11 § 9 LSE. Skatteverket’s narrower definition was rejected. The same reasoning applies to colocation — if mining qualifies, colocation does too.

Commission v. Sweden (2025)

Pending referral · May 2025. The EU Commission referred Sweden to the CJEU for discriminatory tax withholding rules (INFR/2023/4007). Not yet decided — but the Commission is already scrutinizing Swedish tax practices. A formal infringement action signals that Sweden’s discriminatory approach is on the EU’s radar.

Riksrevisionen Audit

Sweden's own auditor confirmed the policy failed. Benefits went to a few large foreign companies. The reform was "not socioeconomically profitable."

Lexel v. Skatteverket (CJEU)

The EU's highest court ruled Sweden's tax rules violated freedom of establishment. Direct precedent for striking down discriminatory Swedish tax measures.

Hedqvist v. Skatteverket (CJEU)

Skatteverket challenged a taxpayer-favorable tax ruling at the CJEU — and lost. The Court held that EU tax exemptions are “independent concepts of EU law” that Member States cannot reinterpret unilaterally. Same procedural path. This precedent supports Projekt Datorhall’s legal theory.

France Proves It Works

France reduced energy tax for ALL data centers — including colocation — under EU-approved GBER rules. Sweden was the only country to discriminate.

Adria-Wien Pipeline (CJEU)

Case C-143/99 · CJEU 2001. Energy tax rebate available only to manufacturing (not services) = selective State aid under Art. 107(1) TFEU. The distinction between goods-producing and service-providing enterprises is not justified by the nature of the tax system. Direct parallel: Sweden grants reduced energy tax to manufacturing but not to data centers.

Keva v. Skatteverket (CJEU)

Case C-39/23 · CJEU 2024. Swedish withholding tax on dividends to foreign public pension funds — while exempting Swedish ones — violates free movement of capital. Skatteverket lost again. The pattern: Sweden repeatedly applies discriminatory tax rules that fail at the CJEU.

Ålands Vindkraft (CJEU)

Case C-573/12 · CJEU Grand Chamber 2014. Sweden’s renewable energy support scheme challenged for restricting free movement of goods. The Grand Chamber confirmed that energy market measures are subject to EU free movement scrutiny and must pass proportionality tests. Sweden’s energy tax discrimination must meet the same standard.

GBER Article 44 Framework

The original tax reduction was authorized under the EU General Block Exemption Regulation Article 44, which permits reductions for energy-intensive users. The framework required equal treatment of comparable facilities. Skatteverket’s reinterpretation violated the scheme’s own terms.

Preliminary opinion by external counsel.

Projekt Datorhall's legal theory has been reviewed by external counsel specializing in Swedish law, EU state aid, and international investment protection. Their preliminary analysis supports the viability of the claims on the following grounds:

Selective advantage to hyperscalers

The 2018 reinterpretation excluded colocation operators while retaining benefits for larger facilities — a potentially selective measure under Article 107(1) TFEU requiring Commission notification.

Energy Tax Act interpretation

HFD 2022 ref. 5 established that cryptocurrency mining qualifies under the data center tax reduction. Skatteverket's narrower interpretation was overturned by Sweden's Supreme Administrative Court.

Quantifiable overpayment

Excluded operators paid the standard rate (~36 öre/kWh) instead of the reduced rate (~0.5 öre/kWh) — a 65x differential. Damages are calculable from electricity consumption records and tax filings.

Full legal opinion available under NDA to qualified participants. This summary does not constitute legal advice.

Who’s on board.

Projekt Datorhall already has active members with documented claims across Europe.

Negotiations ongoing with additional claimants.

Leadership

Dzianis Kryvashei

Owner of KikoSpace AG (CHE-113.539.846), Glarus, Switzerland. Track record of winning precedent-setting cases in Sweden that local lawyers refused to take.

Education. Experience. Results.

See more at kda.vc

Diploma independently verifiable at verify.unisg.ch

“I don’t just research claims — I execute them. Here’s proof.”

Media Coverage

Professional structure, not a startup.

Projekt Datorhall is organized with dedicated roles across legal, financial, and operational functions — standard practice for institutional litigation vehicles.

Dzianis Kryvashei

KDA & Partners (Switzerland). Operational leadership, strategy execution, coordination of all three pillars.

Data Center Sector

Claimants (victims of the 2018 reinterpretation) and investors in Swedish data centers. Onboarding participants with documented claims.

Legal Advisory

Selection and engagement of external counsel. Swedish energy tax law, EU state aid & competition, international arbitration (ECT/BITs).

Litigation Funding

Institutional litigation funder. Due diligence, case evaluation, and full financial backing on a no-win, no-fee basis.

SPV Ownership Structure

Projekt Datorhall operates through a dedicated Swiss Special Purpose Vehicle (SPV) — a separate, ring-fenced entity built exclusively for this litigation.

| Stakeholder | Equity | Role |

|---|---|---|

| Litigation Funder | 60% | Funds all major legal costs. Assumes 100% financial risk. No-win, no-fee. |

| Investors | 20% | Assign claims to SPV. Equity distributed pro rata to documented damages. |

| Management | 20% | Founded the SPV. Operational leadership, legal strategy, and coordination. |

Preliminary. Final structure to be determined upon SPV incorporation.

8 years. Zero challenges filed. We’re changing that.

Despite clear discrimination documented by Sweden’s own auditor, nobody has built a systematic legal case. Not the affected operators. Not the European Data Centre Association (EUDCA). Only political disputes, industry complaints, and parliamentary debates. Projekt Datorhall is the first attempt to build a comprehensive, multi-pathway legal challenge.

Projekt Datorhall is operated by KDA & Partners (Switzerland) through a dedicated Swiss SPV — a separate, ring-fenced vehicle built exclusively for this litigation.

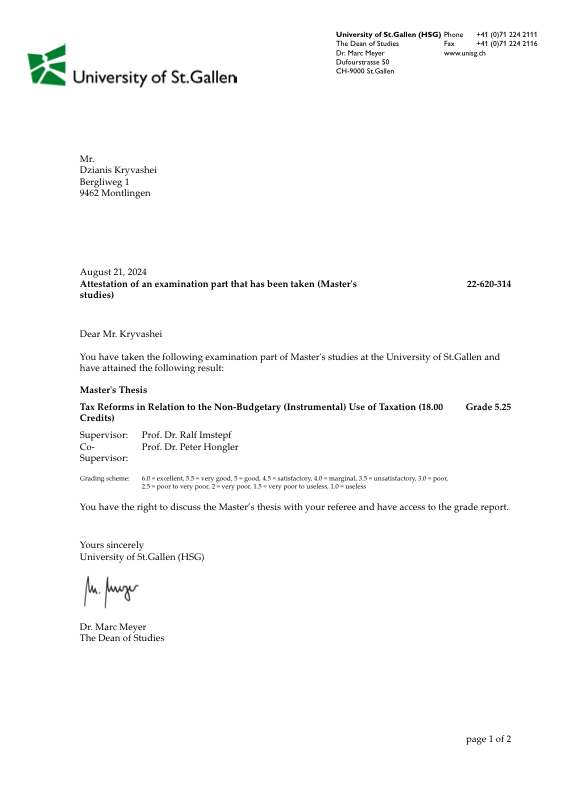

Projekt Datorhall is led by Dzianis Kryvashei — MA in International Law, University of St. Gallen (HSG), Switzerland. A qualified lawyer and insolvency practitioner with specialist training in EU regulatory frameworks. An insolvency practitioner with direct experience recovering assets in Swedish proceedings, including cases initially assessed as unrecoverable.

Purpose-Built Litigation Vehicle

Projekt Datorhall operates through a dedicated Swiss SPV — ring-fenced from other activities. Claimants assign their claims to the SPV and receive equity proportional to their documented damages. Clean, transparent, investor-ready.

Won Where Others Wouldn't Try

Swedish lawyers told us our cases were unwinnable. We achieved multiple legal precedents in Sweden over the past three years — including full debt recovery through bankruptcy proceedings (Bräcke Fastigheter, 2023).

EU-First, Not Sweden-First

62% of Swedish tax attorneys report systemic bias in administrative courts toward Skatteverket (source: Rättvis Skatteprocess, 2023). Projekt Datorhall's strategy therefore focuses on EU-level proceedings — the European Commission and CJEU — where Sweden has an unfavorable track record in comparable tax cases.

International Law, Not Local Caution

MA in International Law from the University of St. Gallen (HSG), Switzerland. Specialized in EU regulatory frameworks. This is not a case for Swedish domestic litigation — it is an EU state aid case, and we are built for it.

We know what Sweden is hiding.

Classified Skatteverket filings reveal the real reasons behind the 2023 abolition and Sweden’s withdrawal from the Energy Charter Treaty. These aren’t public. Sweden never intended them to be. We obtained them. We analyzed them. And they form the backbone of our case.

We Hold Everyone Accountable

Our investigation uncovered that Swedish law firms provided unprofessional services to data center operators, contributing to an estimated €100M in VAT leaks and triggering legal disputes against the very operators they were supposed to protect.

| Swedish Law Firm | Projekt Datorhall Litigation Pool | |

|---|---|---|

| Your cost | €50,000–200,000+ per company | €10,000 — litigation funder covers the rest |

| If you lose | You pay everything | Funder absorbs all costs — no-win, no-fee |

| Forum | Swedish courts — 62% of tax attorneys say biased toward Skatteverket | EU Commission + CJEU — established precedent |

| Claim strength | One company, one claim — easy to ignore | Pooled portfolio — growing coalition worldwide |

| Track record against Skatteverket | Advised clients not to fight | Won cases Swedish lawyers called impossible |

| Conflict of interest | Same firms that gave bad advice now want your case | Independent — we also hold advisors accountable |

| Structure | Hourly billing, no alignment | SPV with shared equity — we win only when you win |

| Legal pathways | Single forum — Swedish courts only | Five parallel pathways — EU Commission, ECT, BITs, Swedish Courts, Förvaltningsrätten |

Two ways to participate.

We designed a two-stage process so you can engage at your comfort level. No binding commitments are required at the initial stage.

Option A — Non-binding registration

Provide basic information to estimate your claim and join the damages pool. No fees, no commitment, no claim assignment.

- Company name and jurisdiction

- Electricity consumption (kWh/year)

- Period affected (2017–2023)

- Claim categories applicable

Purpose: estimate the damages pool and demonstrate portfolio scale to funders.

Option B — Binding claim assignment

Formally assign your claims to the SPV and receive equity proportional to your documented damages. EUR 10,000 membership covers operational costs.

- Claim assignment agreement signed

- Equity in SPV proportional to damages

- External counsel review completed

- Funding agreement in place

Binding participation only after: funding secured, counsel confirmed, eligibility assessed.

Process overview

Book a Call

Confidential discussion under mutual NDA. We assess your situation and identify applicable claim categories.

Register Your Interest

Non-binding registration. Provide electricity data and affected period. Receive the Projekt Datorhall Memorandum with full legal analysis.

Portfolio Assembly

As registrations grow, we present the portfolio to the litigation funder for due diligence and formal funding agreement — covering all five legal pathways.

Litigation & Recovery

Once funded, participants who opt in assign claims to the SPV. EU Commission complaint and national proceedings filed. Recovery distributed pro rata.

How third-party funding works.

Most operators have never used litigation funding. Here is how the process works — and why it exists.

Portfolio assembled

Projekt Datorhall aggregates claims and builds a portfolio with documented damages, legal theory, and supporting evidence.

Funder due diligence

The litigation funder independently evaluates the legal merits, damages quantum, enforcement prospects, and expected timeline.

Funding agreement signed

If approved, the funder commits capital to cover all legal costs. Terms are fixed before any claims are assigned.

Litigation filed

EU Commission complaint and/or national proceedings initiated. The funder bears 100% of the financial risk. If the case fails, participants owe nothing.

Projekt Datorhall is in discussions with institutional litigation funders who specialize in multi-jurisdictional EU proceedings. Funder identity will be disclosed to participants before any binding commitment.

What we do, day by day.

Projekt Datorhall is not a passive holding structure. It is an active operational vehicle with defined workstreams running in parallel.

Claimant intake & documentation

Structured intake process: electricity consumption data, tax filings, corporate structure, affected periods. Each claim documented and categorized across all five pathways.

Counsel coordination

Managing external counsel across Swedish tax, EU state aid, and international arbitration. Coordinating legal opinions, filing schedules, and evidence assembly.

Funder liaison & due diligence

Building the damages portfolio for institutional litigation funders. Preparing due diligence packages, financial models, and risk assessments to secure funding commitments.

Progress & transparency

Regular updates to all participants: case progress, funder status, legal milestones, and financial reporting. Full transparency through the SPV governance structure.

What you should know before joining.

Projekt Datorhall is transparent about the uncertainties involved. Prospective participants should consider the following before making any commitment.

No guarantee of filing or recovery

Litigation may not proceed if funding, participant thresholds, or legal conditions are not met. There is no guarantee of any financial recovery.

Multi-year proceedings

EU state aid litigation typically takes 3–5 years. Participants should not expect near-term results. Delays and procedural setbacks are possible.

Recovery depends on enforcement

Even a favorable ruling requires enforcement proceedings. Collection from sovereign entities involves additional legal and practical challenges.

Individual claim assessment required

Not all claims will qualify. Eligibility depends on specific circumstances, documentation, and applicable limitation periods. Assessment is made after consultation.

Funder terms affect net recovery

Litigation funders receive equity in the SPV in exchange for covering costs. Net recovery to claimants depends on the final funding terms and total costs incurred.

Claims assigned to SPV

Participants assign their claims to the litigation vehicle. This means the SPV — not the individual — controls the legal strategy and settlement decisions.

Adverse publicity risk

Challenging a sovereign state's tax authority may attract attention. Participants should consider reputational implications for their business.

Past rulings do not guarantee outcomes

While Skatteverket has lost comparable cases at the CJEU and in Swedish courts, each case is assessed on its own facts. Prior outcomes are not predictive.

What happens next.

A clear timeline so participants know what to expect at each stage.

Your doubts, addressed.

SPV stands for Special Purpose Vehicle — a Swiss-registered company created exclusively to pursue the Projekt Datorhall litigation. It owns the assigned claims, manages the legal proceedings, receives any recovery, and distributes it to stakeholders according to their equity share. The SPV is ring-fenced from all other activities, which is standard practice in litigation funding.

Four categories: (1) Energy tax claims — discriminatory exclusion from the 97% reduction; (2) VAT recovery claims — non-refund of input VAT on mining and data center operations; (3) Claims against law firms and consultants who provided incorrect strategies; (4) Claims against landlords and local partners who seized equipment, locked facility access, or failed contractual obligations — pursued through Swedish courts. You may have claims in one or multiple categories.

Colocation operators, cryptocurrency mining operators, investors who funded data center projects based on the promised tax regime, companies that went bankrupt due to the tax changes, and anyone who suffered losses from bad advice by Swedish lawyers or consultants regarding data center tax structures. If you were affected between 2017 and 2023, you likely qualify.

EUR 10,000. Flat fee, same for all members regardless of company size. This covers shared legal counsel, EU filings, expert reports, and coordination. Major litigation costs are covered by the litigation funder — not by you.

The litigation funder absorbs all major legal costs. Your maximum exposure is the EUR 10,000 membership fee. No additional costs, no tax liabilities.

Our research identifies at least 10 cases where Skatteverket's position was overruled — including by the CJEU (Lexel, Hedqvist), the Swedish Supreme Administrative Court on the same Energy Tax Act (HFD 2022 ref. 5), and enforcement proceedings where the state was ordered to pay. Projekt Datorhall pursues five parallel legal pathways — EU Commission complaint, Energy Charter Treaty arbitration, bilateral investment treaty claims, Francovich damages, and förhandsbesked — so a setback in one forum does not end the case. Past outcomes do not guarantee future results, but the pattern of adverse rulings and the breadth of legal avenues support the strategy.

No. Swedish tort claims have a 10-year prescription period. The discrimination began in September 2018 — claims remain viable through at least 2028. The abolition occurred in July 2023 — those claims are viable through 2033. EU Commission complaints have no formal time limit. But earlier is better — act now.

No. This is one of the most important facts. Despite clear discrimination and documented damage, no formal EU state aid complaint has ever been filed and Skatteverket's 2018 position statement was never challenged in court. The Finance Minister herself acknowledged it "could be subject to court review." Projekt Datorhall would be first movers.

The litigation funder receives 60% equity in the SPV in exchange for funding all major litigation costs — hundreds of thousands of euros upfront with no guarantee. EU state aid litigation is complex, multi-jurisdictional, and takes 3–5 years. If the case fails, they absorb the loss entirely. The 60% share reflects high risk, long timelines, and substantial capital commitment. Without third-party funding, each investor would need EUR 20,000–50,000+ individually.

For context: one hour of EU state aid legal counsel costs EUR 400–800. An individual legal challenge costs EUR 50,000–200,000+. The annual energy tax loss for a 5MW colocation facility was EUR 200,000–600,000. EUR 10,000 gives you access to shared EU-level legal representation that would cost EUR 13,000–35,000+ independently — plus classified documents not available at any price.

Realistic timeline: pool formation in 3–6 months, EU Commission complaint filed within a year, ECT arbitration initiated within 12–18 months, preliminary tax ruling pursued in parallel, and primary resolution in 3–5 years. All five pathways run in parallel, not sequentially. Interest accrues on damages, so delayed resolution increases recovery.

The Energy Charter Treaty is an international investment treaty that protects energy-sector investors against unfair treatment by host states. Sweden ratified the ECT and, despite the EU’s collective withdrawal in 2025, the ECT’s 20-year sunset clause means its protections remain in force until 2045. Projekt Datorhall can initiate arbitration under Article 26 ECT, arguing that Sweden’s regulatory reversal constitutes a breach of fair and equitable treatment (FET), indirect expropriation, and discriminatory measures against foreign data center investors.

In May 2025, Sweden’s own Supreme Court (Högsta domstolen, T 555-24) confirmed that ECT arbitration remains valid for third-country (non-EU) investors, even where intra-EU claims are barred under CJEU Komstroy. This directly validates the Swiss SPV approach.

BITs are agreements between two countries that protect cross-border investors from unfair treatment. Sweden has an extensive BIT network — the UNCTAD Investment Policy Hub lists dozens of treaties. If a Projekt Datorhall claimant invested from a country that has a BIT with Sweden, they may have an independent arbitration claim for breach of investment protections. Projekt Datorhall evaluates each participant’s nationality and investment structure to identify applicable BITs, adding another parallel pathway to the EU and ECT tracks.

Absolutely. Small operators may have the strongest moral case — customers under 100kW were completely excluded. In a litigation pool, your costs are EUR 10,000 regardless of size. Your claim adds to aggregate damages, making the case more attractive to funders. Every participant strengthens the coalition.

What you’d pay to build this yourself.

Independent legal research for a case of this complexity requires multiple specialist opinions. Here’s what the market charges.

| Item | Market rate |

|---|---|

| EU state aid legal opinion | €5,000–15,000 |

| ECT arbitration assessment | €3,000–8,000 |

| BIT eligibility analysis | €2,000–5,000 |

| Classified document access | Not available |

| Damage model construction | €3,000–7,000 |

| Total | €13,000–35,000+ |

All of the above. Plus shared litigation. Plus the documents Sweden never wanted you to see.

Projekt Datorhall Memorandum

Our comprehensive legal analysis, damage calculations, EU precedent mapping, and strategic roadmap — the most detailed document ever produced on this case. Exclusively for qualified participants.